Global Cell Therapy Bioprocessing Market Trends 2026–2034 | 13.49% CAGR & Competitive Scenario

The Cell Therapy Bioprocessing industry supports the development of next generation medical treatments by providing technologies and systems for cell isolation, culture, expansion, and formulation. It enables the transition of innovative therapies from laboratory research to commercial production.

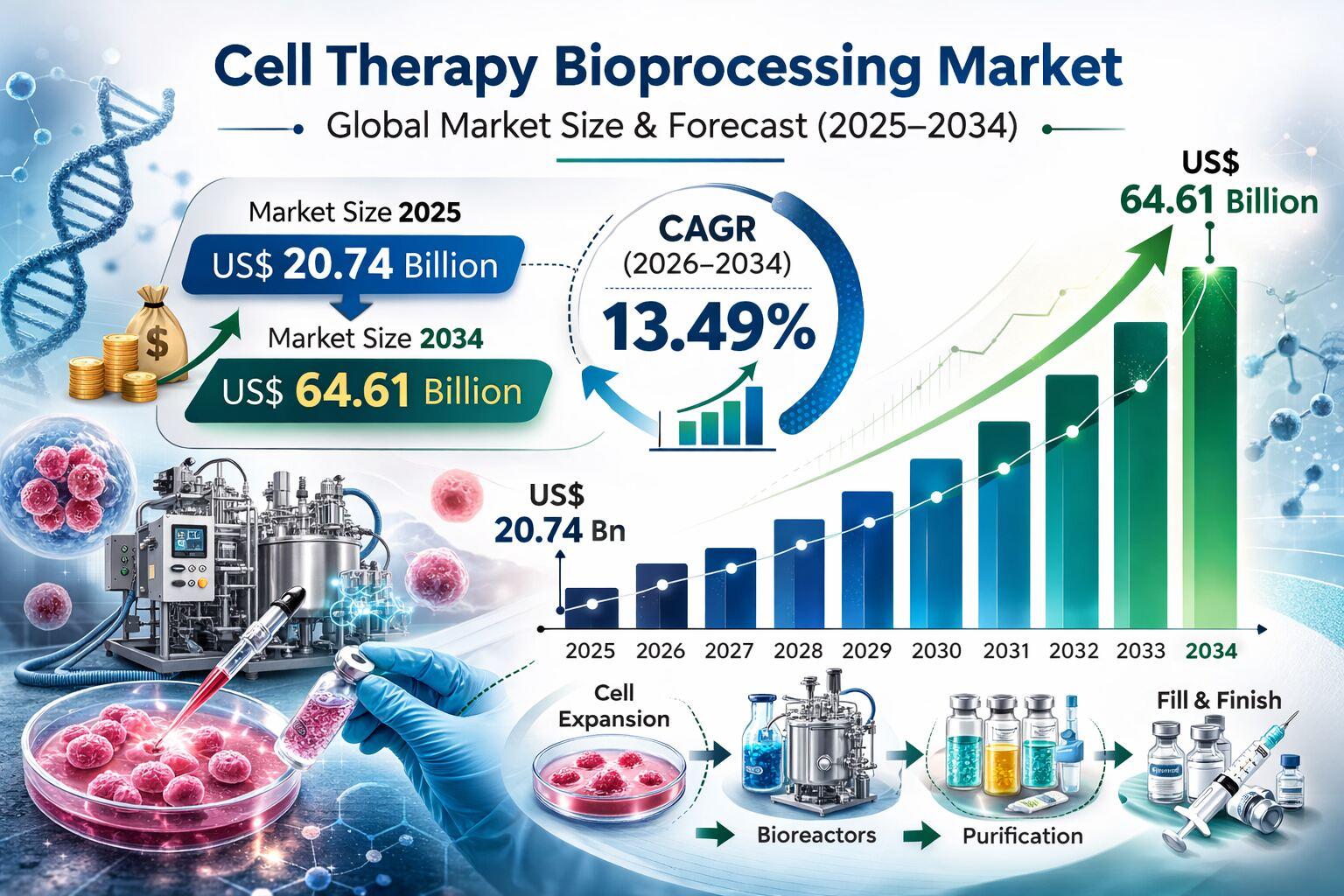

Cell Therapy Bioprocessing Market Analysis

The Cell Therapy Bioprocessing Market is poised for remarkable expansion, with its size projected to grow from US$ 20.74 billion in 2025 to US$ 64.61 billion by 2034, registering a robust CAGR of 13.49% during 2026 to 2034. This strong trajectory reflects the rapid transition of cell and gene therapies from experimental pipelines to commercial reality. As advanced therapies gain regulatory approvals and clinical acceptance, the demand for scalable, compliant, and cost efficient manufacturing platforms continues to intensify.

Technological innovation remains central to market acceleration. The widespread adoption of single use bioreactors has improved operational flexibility and minimized cross contamination risks. Automation and robotics are increasingly integrated into upstream and downstream processes to enhance precision and reduce manual intervention. Artificial intelligence driven analytics are also transforming process monitoring, enabling real time optimization and predictive quality control. These advancements collectively strengthen production efficiency and reduce batch failure risks.

Market Overview

Cell therapy bioprocessing encompasses the complete workflow required to develop and manufacture therapeutic cells under strict Good Manufacturing Practice conditions. This includes cell sourcing and isolation, expansion and culture, harvesting, purification, formulation, and cryo preservation for storage and distribution. The process is highly sensitive, requiring rigorous quality control and validated infrastructure.

Therapeutic categories such as mesenchymal stem cells, induced pluripotent stem cells, hematopoietic stem cells, and immune cells including CAR T cells represent the primary focus of manufacturing pipelines. A notable market shift is underway from patient specific autologous therapies toward standardized allogeneic platforms. Allogeneic therapies offer off the shelf availability and improved scalability, which demand robust and reproducible manufacturing systems. This transition is driving investments in modular, closed system facilities and high throughput processing technologies.

Market Drivers and Opportunities

The rising global prevalence of chronic and life threatening diseases significantly contributes to market demand. Oncology remains the largest indication, particularly with the growing adoption of CAR T and adoptive T cell therapies. Cardiovascular disorders, orthopedic conditions, and wound healing applications further broaden therapeutic scope.

Rising research and development investments from both private and public sectors support clinical trials and manufacturing infrastructure expansion. Government initiatives aimed at regenerative medicine and advanced therapy medicinal products are accelerating commercialization pathways. Regulatory agencies are increasingly offering fast track and breakthrough designations for innovative therapies, further supporting market growth.

Opportunities are expanding in emerging economies across Asia Pacific, where healthcare infrastructure is improving and patient awareness is rising. The growing role of Contract Development and Manufacturing Organizations offers scalable service models for biotechnology firms seeking commercial production support. Integration of process analytical technologies and digital twins creates additional opportunities to enhance yield, optimize cost of goods sold, and standardize quality outcomes.

Download Sample PDF : https://www.theinsightpartners.com/sample/TIPRE00021550

Segmentation Analysis

The market is segmented by technology, cell type, indication, end user, and geography.

By technology, key segments include bioreactors, lyophilization systems, electrospinning, control flow centrifugation, ultrasonic lysis, genome editing technology, cell immortalization technology, and viral vector technology. Bioreactors dominate due to their central role in large scale cell expansion.

By cell type, the market covers stem cells, immune cells, human embryonic stem cells, pluripotent stem cells, and hematopoietic stem cells. Immune cells represent a high growth segment driven by oncology applications.

By indication, oncology leads, followed by cardiovascular disease, wound healing, and orthopedic disorders. By end user, hospitals and clinics, regenerative medicine centers, academic and research institutes, and diagnostic centers form the core demand base.

Regional Insights

North America holds the largest market share, supported by advanced healthcare infrastructure, strong venture capital funding, and regulatory support. The region benefits from high concentration of biotechnology firms and rapid adoption of automated manufacturing systems.

Europe maintains a significant share due to strong public funding mechanisms and harmonized regulatory frameworks for advanced therapy medicinal products. Collaborative research networks and academic excellence strengthen the regional ecosystem.

Asia Pacific is projected to record the fastest growth rate. China, India, and Japan are investing heavily in GMP compliant manufacturing facilities and automation technologies. Cost advantages and expanding patient populations enhance regional competitiveness.

South and Central America and the Middle East and Africa represent emerging markets with growing investments in healthcare modernization and early stage adoption of scalable closed systems.

Competitive Landscape and Key Players

The market is highly competitive, characterized by strong participation from global life science tool providers and specialized manufacturing service companies. Key players focus on automation, closed system development, strategic partnerships, and facility expansion.

Major Companies Operating in the Market:

-

Thermo Fisher Scientific Inc.

-

Sartorius AG

-

Lonza

-

Merck KGaA

-

Cytiva

-

Corning Incorporated

-

Fresenius Kabi AG

-

Asahi Kasei Corporation

-

Repligen Corporation

-

Catalent Inc

These companies leverage integrated solutions across the cell therapy value chain, including equipment supply, media development, viral vector production, and end to end CDMO services.

Future Outlook

The future of the cell therapy bioprocessing market is defined by industrialization, digital transformation, and global expansion. As allogeneic therapies move closer to large scale commercialization, standardized and automated manufacturing platforms will become essential. Artificial intelligence, real time analytics, and advanced process modeling are expected to significantly enhance production consistency and regulatory compliance. Strategic collaborations between biotechnology innovators and manufacturing service providers will further accelerate therapy availability worldwide. With sustained investment, supportive regulatory frameworks, and expanding clinical pipelines, the market is positioned for sustained double digit growth through 2034.

Other Reports :