E-Voting Technology Concerns: eSlate System Issues

Games |

2025-09-18 02:13:34

The landscape of auto insurance is undergoing a seismic shift, and one of the most exciting innovations on the horizon is Usage-Based Motor Insurance (UBI). While national insurers like Progressive and Allstate have been at the forefront of this change, regional insurers are now poised to take full advantage of UBI car insurance as a way to deliver more personalized, data-driven policies. As technology evolves and consumer demands shift, this form of auto insurance presents a significant opportunity for regional carriers to improve customer engagement, increase retention, and compete with larger, more established companies.

Here’s how regional insurers can tap into the growing usage-based motor insurance market and drive success in the years ahead.

The Growth of Usage-Based Motor Insurance (UBI)

The usage-based motor insurance market has seen explosive growth over the last few years, and the trend shows no signs of slowing down. In fact, the global UBI market is projected to grow from $43.38 billion in 2023 to $70.46 billion by 2030, driven by an increasing consumer appetite for personalized insurance pricing based on driving behavior rather than static risk models.

While large, national carriers have been quick to adopt UBI car insurance offerings, regional insurers have largely been slower to jump on the bandwagon. Historically, regional players have faced high entry costs and the challenge of integrating complex telematics systems into their operations. However, the evolution of smartphone-based UBI solutions has dramatically reduced these barriers, making it easier for smaller insurers to step into the market.

How Smartphone-Based UBI is Changing the Game

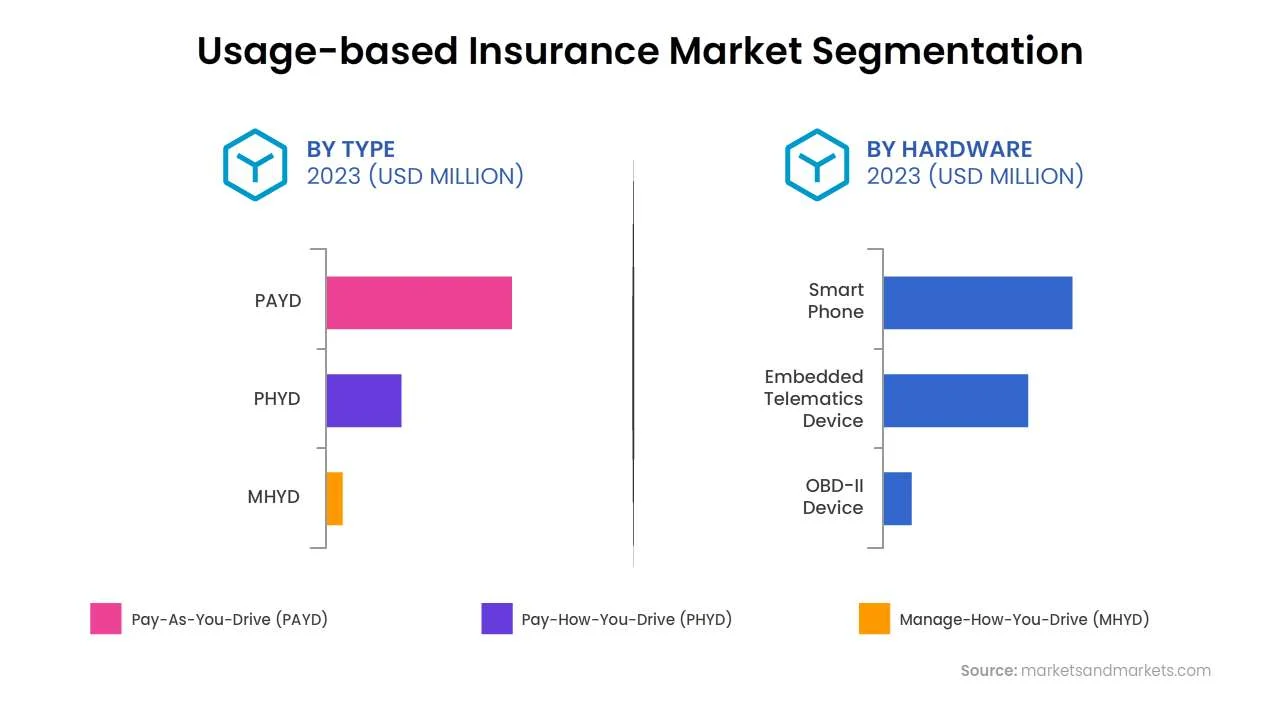

Traditionally, UBI car insurance relied on specialized hardware like OBD (on-board diagnostics) devices to collect driving data. These devices, while effective, came with high installation costs and the need for physical equipment in every vehicle. However, in recent years, smartphone-based telematics has emerged as a cost-effective alternative. With nearly 75% of new cars sold in 2024 expected to have built-in connectivity, insurers now have access to vast amounts of real-time driving data via smartphones—without the need for additional devices.

For regional insurers, this shift is a game changer. The adoption of smartphone-based telematics makes it possible to offer usage-based motor insurance without requiring the investment in expensive hardware. Insurers can instead focus on building user-friendly apps and data analytics capabilities to assess driver behavior and offer personalized, usage-based pricing. This makes UBI car insurance much more accessible to regional players who are keen to tap into the growing demand for flexible, usage-based policies.

Regional Carriers: Leveraging Local Insights for Better UBI Offers

One of the biggest advantages that regional carriers have over national players is their deep understanding of local markets. National insurers may struggle to tailor products to specific regional nuances, but regional carriers can craft usage-based motor insurance policies that reflect the unique driving patterns, weather conditions, and risks in their local communities.

For example, a regional insurer operating in a rural area could offer discounts for low-mileage drivers, recognizing that these customers present a lower risk. Similarly, insurers in areas prone to heavy snowfall could create policies that adjust pricing based on driving behavior during winter months. This local expertise is difficult for national insurers to replicate and offers regional players a valuable edge in the UBI car insurance market.

A real-world example of this is Ohio Mutual Insurance, which launched a smartphone-based usage-based motor insurance program tailored to young, rural drivers. By analyzing local driving data, they were able to provide personalized pricing that resonated with their target audience, resulting in improved customer engagement and higher retention rates. This is exactly the kind of localized, data-driven approach that regional insurers can use to differentiate themselves in the UBI car insurance space.

Regulatory Sandboxes: A Hidden Advantage for Regional Insurers

Another advantage for regional insurers is the growing number of states that are offering regulatory sandboxes for insurance innovation. States like Arizona, Kentucky, and Pennsylvania have introduced relaxed regulatory frameworks that allow insurers to test usage-based motor insurance products without the burden of complying with every traditional regulatory requirement.

These innovation-friendly programs make it easier for regional carriers to experiment with new products, including UBI car insurance, and refine them before launching on a larger scale. This gives smaller insurers a unique opportunity to innovate faster and more effectively than their larger counterparts, who may face more rigid compliance requirements.

States like Ohio, Texas, and Pennsylvania have launched their own versions of these regulatory sandboxes, allowing insurers to introduce UBI car insurance solutions with fewer regulatory hurdles. This is particularly important for regional insurers who may not have the resources to navigate the complexities of state-specific insurance laws but can benefit from these relaxed testing conditions to fine-tune their offerings.

The Path to Success: A Tailored Approach to UBI Car Insurance

For regional insurers looking to succeed in the usage-based motor insurance market, the key is to focus on personalization. By leveraging smartphone-based telematics, regional carriers can gather and analyze data on driver behavior in ways that were previously impossible. This allows them to offer more accurate, dynamic pricing based on actual usage and individual driving habits.

At the same time, regional insurers have the unique advantage of being able to tailor their UBI car insurance offerings to the specific needs of their communities. Whether it’s adjusting rates based on local road conditions, offering discounts for safer driving behaviors, or catering to niche demographics like young or rural drivers, regional insurers can craft highly personalized policies that larger carriers simply can’t replicate.

Additionally, the favorable regulatory environment in many states is a key factor that enables regional players to enter the usage-based motor insurance market quickly and efficiently. By taking advantage of these innovation sandboxes, regional insurers can refine their UBI products, build customer trust, and scale their operations without facing the regulatory roadblocks that often slow down larger competitors.

Conclusion: Regional Insurers Have the Advantage in UBI Car Insurance

The usage-based motor insurance market is growing at a rapid pace, and regional insurers are in a prime position to capitalize on this shift. By leveraging smartphone-based telematics, tapping into local knowledge, and taking advantage of regulatory sandboxes, regional insurers can deliver personalized, data-driven UBI car insurance solutions that meet the needs of today’s consumers.

In the fast-evolving world of auto insurance, usage-based motor insurance is more than just a trend—it’s the future. Regional insurers who embrace this technology will be well-positioned to compete with larger carriers, engage customers with more personalized offerings, and carve out a niche in this rapidly expanding market.

The question is no longer if regional insurers should adopt UBI car insurance but when. The time is now to innovate, personalize, and lead the way in the usage-based motor insurance revolution.